The author is an economist with Ag Business Solutions and a market analyst for the Daily Dairy Report.

Global demand for dairy products remains strong. As a result, international factors are playing a larger role in determining milk prices. But farm-level profits - or losses - are still a local matter.

China's voracious appetite for milk powders has largely driven global dairy demand. In 2012, Chinese skim and whole milk powder imports were 27 percent greater than the previous year. Through this July, imports are 24 percent higher than the same period in 2012. As the middle class in China and other emerging markets continues to expand, demand for milk powders will likely rise as well.

In recent years, higher global dairy product demand has outpaced supply growth. That was exacerbated this year by a crippling drought in New Zealand and unfavorable weather and farm-level economics throughout Europe.

Reduced output from the United States' largest competitors in the export market created a vacuum, and U.S. dairy exports are larger than they have ever been. Exports have consumed more than 15 percent of this year's milk solids production and more than half of domestic milk powder.

U.S. dairy product prices remain at a sizeable discount to prices overseas, which has helped put a floor under domestic prices and suggests U.S. exports will remain strong for months.

Competition next year may be stiffer. Processors overseas have promised very high payouts, and this, coupled with lower feed prices, will encourage more milk production. New Zealand's season is off to a robust start. Fonterra reported a 5 percent expansion in milk collections in New Zealand compared to the first three months of the 2012 to 2013 season. Pasture growth is excellent, and milk production is expected to remain strong, weather permitting.

Still, global dairy product stocks are low, and Europe and New Zealand will need to rebuild inventories. Dairy product prices are likely to be lower next year, as global milk production rebounds. Prices may not truly capitulate, though, until U.S. competitors rebuild inventories and are forced to push large volumes of product onto the market. This prospect remains months away, at least, and may not happen if weather sours.

Grain prices falling

Will projected milk prices be enough to cover producers' costs? In many regions, the answer is a resounding yes. Feed costs for all domestic producers are finally abating. Corn futures have fallen more than 40 percent from their previous year highs. USDA expects the corn crop to reach 13.84 billion bushels, which would be record-large production despite a national average yield that falls short of the trend line. This suggests that there is room for lower U.S. corn acreage and still plentiful - and affordable - grain supplies in years to come.

With corn prices near the cost of production, the substantial advantage that farming dairy producers held over their feed-buying counterparts will dissipate.

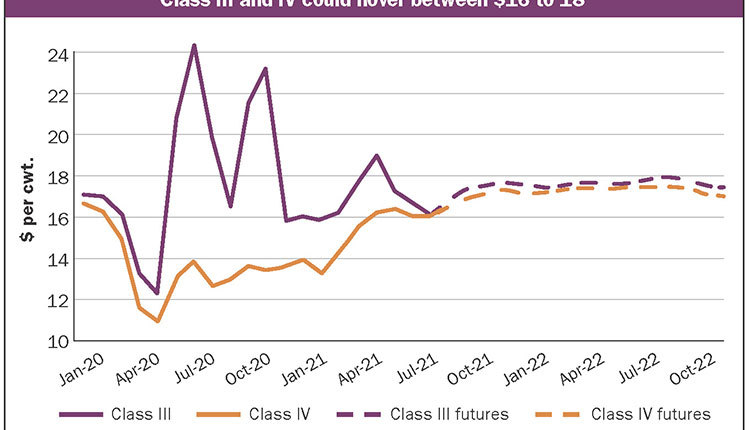

Class III futures are currently forecasting a payout of $16 or $17 per cwt., high enough to pay the bills in the Midwest and Northeast, where forage and grain prices are much lower than they were a few months ago.

The only cost that remains elevated for these producers is soybean meal. Soybean prices remain strong due to dry conditions in the pod-filling stage. Substitutes including canola are readily available, and by spring, the market could be pressured lower by soybeans from South America.

For some producers, the mirage that all feed prices will decline this autumn has shimmered and vanished. Years of drought have reduced forage supplies to minimal levels, and prices for hay and corn silage in the Southwest are stubbornly high. If the drought continues to recede, higher hay production in the spring could pressure prices in much of the region.

In California, forage prices will likely remain high. Precious water and acreage continue to shift away from corn and hay to higher-value crops like vegetables, citrus, nuts and grapes. For the foreseeable future, dairy producers in the Golden State must either pay a steeper price for corn silage or continue to lose acreage to almonds and tomatoes. California producers who grow forage will enjoy lower feed costs but they must forgo the opportunity to earn more with cash crops.

Better cash flow ahead

Mailbox milk prices are also a local issue. Producers in areas with heavy Class IV (dry powder, whey and butter) utilization will continue to enjoy a larger milk check than their counterparts whose pay price is based solely on the much lower Class III (cheese) price. Expansion in the industry has been concentrated in the Midwest, which suggests cheese production will remain strong. This could sustain a Class III discount to Class IV prices.

For most producers, the future is bright. Global demand is firm, and it will take time to rebuild dairy product inventories. With several years of sexed semen usage and following more than a year of very high cull rates, domestic expansion could be limited by tight heifer supplies. The lofty milk prices seen earlier this year are probably out of reach, but with lower feed costs, they won't be needed. The industry will likely realize a period of sustained profitability at a milk price that keeps both producers and consumers happy.

This article appears on page 657 of the October 10, 2013 issue of Hoard's Dairyman.

Global demand for dairy products remains strong. As a result, international factors are playing a larger role in determining milk prices. But farm-level profits - or losses - are still a local matter.

China's voracious appetite for milk powders has largely driven global dairy demand. In 2012, Chinese skim and whole milk powder imports were 27 percent greater than the previous year. Through this July, imports are 24 percent higher than the same period in 2012. As the middle class in China and other emerging markets continues to expand, demand for milk powders will likely rise as well.

In recent years, higher global dairy product demand has outpaced supply growth. That was exacerbated this year by a crippling drought in New Zealand and unfavorable weather and farm-level economics throughout Europe.

Reduced output from the United States' largest competitors in the export market created a vacuum, and U.S. dairy exports are larger than they have ever been. Exports have consumed more than 15 percent of this year's milk solids production and more than half of domestic milk powder.

U.S. dairy product prices remain at a sizeable discount to prices overseas, which has helped put a floor under domestic prices and suggests U.S. exports will remain strong for months.

Competition next year may be stiffer. Processors overseas have promised very high payouts, and this, coupled with lower feed prices, will encourage more milk production. New Zealand's season is off to a robust start. Fonterra reported a 5 percent expansion in milk collections in New Zealand compared to the first three months of the 2012 to 2013 season. Pasture growth is excellent, and milk production is expected to remain strong, weather permitting.

Still, global dairy product stocks are low, and Europe and New Zealand will need to rebuild inventories. Dairy product prices are likely to be lower next year, as global milk production rebounds. Prices may not truly capitulate, though, until U.S. competitors rebuild inventories and are forced to push large volumes of product onto the market. This prospect remains months away, at least, and may not happen if weather sours.

Grain prices falling

Will projected milk prices be enough to cover producers' costs? In many regions, the answer is a resounding yes. Feed costs for all domestic producers are finally abating. Corn futures have fallen more than 40 percent from their previous year highs. USDA expects the corn crop to reach 13.84 billion bushels, which would be record-large production despite a national average yield that falls short of the trend line. This suggests that there is room for lower U.S. corn acreage and still plentiful - and affordable - grain supplies in years to come.

With corn prices near the cost of production, the substantial advantage that farming dairy producers held over their feed-buying counterparts will dissipate.

Class III futures are currently forecasting a payout of $16 or $17 per cwt., high enough to pay the bills in the Midwest and Northeast, where forage and grain prices are much lower than they were a few months ago.

The only cost that remains elevated for these producers is soybean meal. Soybean prices remain strong due to dry conditions in the pod-filling stage. Substitutes including canola are readily available, and by spring, the market could be pressured lower by soybeans from South America.

For some producers, the mirage that all feed prices will decline this autumn has shimmered and vanished. Years of drought have reduced forage supplies to minimal levels, and prices for hay and corn silage in the Southwest are stubbornly high. If the drought continues to recede, higher hay production in the spring could pressure prices in much of the region.

In California, forage prices will likely remain high. Precious water and acreage continue to shift away from corn and hay to higher-value crops like vegetables, citrus, nuts and grapes. For the foreseeable future, dairy producers in the Golden State must either pay a steeper price for corn silage or continue to lose acreage to almonds and tomatoes. California producers who grow forage will enjoy lower feed costs but they must forgo the opportunity to earn more with cash crops.

Better cash flow ahead

Mailbox milk prices are also a local issue. Producers in areas with heavy Class IV (dry powder, whey and butter) utilization will continue to enjoy a larger milk check than their counterparts whose pay price is based solely on the much lower Class III (cheese) price. Expansion in the industry has been concentrated in the Midwest, which suggests cheese production will remain strong. This could sustain a Class III discount to Class IV prices.

For most producers, the future is bright. Global demand is firm, and it will take time to rebuild dairy product inventories. With several years of sexed semen usage and following more than a year of very high cull rates, domestic expansion could be limited by tight heifer supplies. The lofty milk prices seen earlier this year are probably out of reach, but with lower feed costs, they won't be needed. The industry will likely realize a period of sustained profitability at a milk price that keeps both producers and consumers happy.